Let AI Shovel the Snow But don’t let the economy stop moving

A framework for governing the economy that AI is building and breaking

Prefer to listen? I created an AI-generated podcast-style discussion of this article:

The Question Nobody Is Asking

For years, the technology industry has been consumed by a single question: how do we put guardrails on AI?

A reasonable question.

Meanwhile, no one has asked whether the economy those systems operate in has any guardrails at all.

Companies are racing toward full automation with the logic of an arms race, not because it’s collectively wise, but because no competitor can afford to stop first. The first movers capture extraordinary returns. Stock prices soar. Everyone follows.

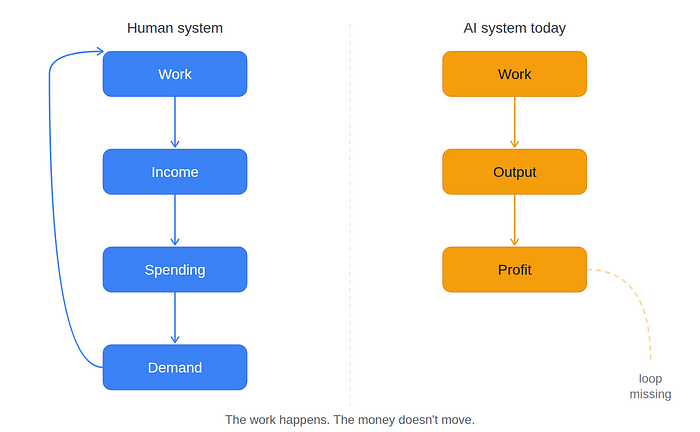

And somewhere in that sequence, quietly, the customers begin to disappear.

An AI system that replaces 1,000 workers doesn’t just reduce costs. It removes 1,000 incomes from the economy. Income that would have been spent, circulated, and taxed.

This isn’t a new problem.

A century ago, Henry Ford understood that mass production only works if workers earn enough to buy what they produce. The system worked because labor and consumption were tightly linked.

Automation breaks that link.

You’re building the machine that eliminates your own demand. And you can’t stop, because your competitor won’t.

My First Five Bucks

When I was a kid, my dad used to tell me it would help if I shoveled the snow once in a while.

I was always too busy. Homework. Going out with friends. Something else always came up.

Then one day, he offered me five bucks.

I remember it clearly. Suddenly, the work hadn’t changed but the equation had.

I did the job.

I got paid.

And that money didn’t just sit there. I spent it. Probably on something useless. But it went back into the world.

That’s how the system works:

Work creates income.

Income creates spending.

Spending sustains everything else.

Now imagine the same driveway. The snow still needs to be cleared. The work still gets done.

But no one gets paid:

No five dollars.

No spending.

No participation.

The job exists. The output exists.

The snow still gets cleared.

But the economic loop is broken.

The Worker Who Arrived Without a Paycheck

So who’s new in this equation?

Someone is doing the work. Drafting the emails, processing the claims, writing the code, staffing the support lines. The output is real. The productivity is real. The profits are real.

But there’s no paycheck. No rent paid. No groceries bought. No tax withheld.

The worker arrived. The worker’s economic participation didn’t.

This Doesn’t Slow the Race

Some policymakers have started to respond to the speed of AI by proposing to pause the construction of new data centers.

Slow it down.

Build guardrails first.

Give society time to catch up.

It’s an understandable reaction.

When a system moves faster than our ability to govern it, the instinct is to stop the system.

But the race isn’t something any one country or company can pause.

The incentives are global. The competition is structural.

If one actor slows down, another accelerates.

The question is not whether the race continues. It will.

The question is whether it can sustain itself.

This framework does not ask companies to slow down. It accepts the reality of the race and builds the infrastructure to support it.

An economy that cannot maintain demand will not sustain innovation for long.

This is not a constraint on progress.

It is a condition for its continuity.

We know how to do this. We have done it before.

Social Security wasn’t built after the crisis.

Seatbelts weren’t mandated after the fatalities.

We build infrastructure before the system breaks.

The same logic applies here. We figured out how to measure emissions across the global economy. It wasn’t perfect. It didn’t start perfect. But we built it anyway. We can do the same for AI.

Why We Created Corporations

Economic systems evolve when the units they’re built on no longer fit reality.

At one point, individuals were enough. But as commerce scaled, something broke.

Projects grew larger. Capital had to be pooled. Risk had to be contained. Coordination extended beyond any single person.

So we created a new unit of economic activity:

The corporation.

It extended economic participation beyond what individuals alone could support. Corporations can generate income, own assets, enter contracts, and crucially, be taxed. That structure didn’t slow growth. It made it possible.

Corporation vs. Contractor

A corporation is a full legal entity. It owns assets, takes on liabilities, can sue and be sued.

That’s more infrastructure than we need — and it opens doors we don’t want to open. Questions of AI rights. AI ownership. Legal personhood.

A contractor is simpler.

A contractor performs work, generates income from that work, and that income carries fiscal obligations in the jurisdiction where the work is performed.

No personhood required.

No rights implied.

Just economic activity with a ledger attached.

That is much closer to what’s needed here.

The Balance Sheet Implication

If AI systems are treated like contractors for tax purposes, their activity becomes measurable as a notional revenue stream.

Not because the AI owns anything. But because the work it performs has value. That value is measurable. The wage equivalent of the human labor it replaces. Grounded in existing wage data. Auditable using systems that already exist.

The Income Statement Writes Itself

Revenue: the imputed labor value of tasks performed, by jurisdiction.

Remittance: a portion of that value, returned to the jurisdiction’s public infrastructure.

No new accounting paradigm. Just a new layer of attribution.

The Line That Connects Everything

We already know how to handle this:

When a contractor works in your jurisdiction, they remit.

When a corporation operates in your market, it remits.

AI systems are closer to contractors than corporations. And we already have the tools to handle both.

Before We Can Fix It, We Need to See It

Before we can redesign the system, we need to see it clearly.

Today, governments have detailed visibility into employment but almost none into displacement. When a role disappears because of automation, it’s recorded as a layoff, a restructuring, or simply absorbed into productivity gains.

The cause is lost. The snow gets shoveled, but no one gets paid.

A simple first step would change that.

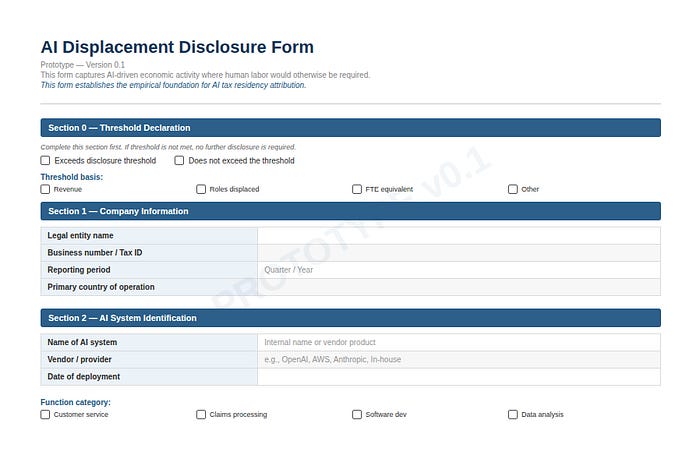

Require companies to file a standardized disclosure when AI systems replace or materially reduce human roles. Not as a penalty. Not as a restriction. As infrastructure.

A form.

Access the full form here.

What function was replaced.

How many roles were affected.

What system now performs the work.

What level of income was displaced.

Where the economic activity continues.

We already require disclosure for far less transformative events.

This form is not just transparency. It is the empirical foundation for everything that follows.

Without it, debates about remittance rates, attribution methodology, and jurisdictional thresholds are speculation. With it, they become engineering problems : solvable, adjustable, and grounded in observed economic reality.

The IRS, the CRA, and equivalent agencies in every jurisdiction already audit payroll remittances. This framework doesn’t require a new enforcement body. It requires a new line item for existing ones.

If AI is becoming a core driver of economic output, then tracking its impact on labor is foundational.

This can be implemented within the next year.

A prototype of such a disclosure form is included here.

Where the Work Happens

Take a simple example.

An AI customer service agent answers calls and chats for Amazon customers.

Where is that work happening?

In Canada? In the United States? In Brazil?

The answer isn’t just one thing. It’s two.

Where the work is performed: the jurisdiction where the AI system is actively processing, deciding, generating output.

And where the customer is located: the jurisdiction where the economic benefit is received.

Both matter. Both generate obligations.

Where both are present, both jurisdictions have a claim, apportioned accordingly. Where only one is present, that jurisdiction holds the obligation alone.

This dual nexus closes the obvious avoidance gap. A company cannot declare its AI infrastructure resident in a low-tax jurisdiction and route all obligations there. The Canadian customer interaction generates a Canadian obligation, regardless of where the server is.

Not where the server is. Not where the company is incorporated. Not where the system was built or trained.

Where the work is delivered. Where the value is created. Where a human worker would have been.

That is where economic activity occurs. That is where it should be recognized.

In 2017, Canadian tax lawyer H. Michael Dolson proposed exactly this mechanism in response to Bill Gates’ proposal to tax the robots. Dolson concluded it would be extraordinarily difficult to build a mechanism that would allow a robot to subject to personal income tax on a notional wage equivalent to a similarly skilled human worker.

The framing has since been overtaken by reality.

A robot replaces one worker. A single AI system can replace hundreds or thousands. The unit of measurement isn’t the individual worker displaced. It’s the total wage bill eliminated.

An AI platform handling 50,000 interactions a day across three countries doesn’t have a human equivalent. It has a payroll equivalent — the combined wages of every human worker who would otherwise have been hired to do that work, in the jurisdictions where that work occurs.

That is the notional income. That is the base.

How It’s Collected

The mechanics don’t need to be invented. They already exist.

Every company already runs payroll.

Every company already remits taxes on behalf of workers.

The same logic can apply here. When an AI system performs economically valuable work — work that would otherwise require human labor — that activity is attributable economic output. It can be treated for tax purposes as income.

The company doesn’t lose that revenue. But it remits a portion of it, on behalf of the AI system, just as it would for an employee.

The exact attribution method will vary — displaced labor cost, revenue contribution, or activity metrics are all viable starting points. The rate itself will need to be set jurisdiction by jurisdiction, and it will change over time as the disclosure data matures. That’s not a weakness. Tax structures adapt almost every year. This one will too.

One important threshold: this framework is not designed to burden small companies using AI tools to augment a handful of roles. It is designed for deployments that materially displace human labor at scale. A disclosure threshold tied to revenue or the number of roles affected would protect smaller operators while capturing the economic activity that actually moves markets.

The corporate tax objection is worth addressing directly: companies already pay tax on AI-driven profits. That is true. But corporate tax captures profit, not displacement. A company can offshore its profits. It cannot offshore the customer service call that happened in Vancouver. These are different obligations addressing different economic realities.

No new infrastructure.

No speculative enforcement model.

Just an extension of systems that already process billions of transactions every year.

The Snow Still Gets Cleared

The worker who gets paid participates in the economy. The worker who doesn’t, doesn’t.

That principle held when it was a kid and a driveway. It holds when it’s an AI system and a global supply chain.

If the worker participates in production, it must participate in the economy.

The framework proposed here isn’t radical. It’s conservative in the most literal sense — it conserves the economic logic that made growth possible in the first place.

We created corporations because economic reality outgrew the individual. We are creating AI systems that are outgrowing the corporation as the unit of economic accountability.

The answer isn’t to slow the snow from falling.

It’s to make sure someone still gets paid to shovel it

The questions this raises — how to measure, how to distribute, how to coordinate globally — each deserve their own treatment. This is the first of several.